The Increasing Use of Insurance in Wealth Management Strategy

February 9, 2023

David Donato, Managing Director, Insurance Solutions

Dan Moore, Managing Director, Insurance Solutions

Insurance solutions are rapidly becoming integral to comprehensive financial planning and wealth management strategies. A recent survey by Accenture of wealth management clients found that over half of respondents want a holistic offering of services that includes risk protection and lending. And over 75% of younger wealth management clients – including the highest income earners – expect their advisors to offer insurance solutions.

Let’s explore the trends driving the demand and growth for insurance solutions in wealth management, and how advisors can use this information to provide better outcomes for their most vital clients.

Why Insurance Solutions are Growing

One of the most significant benefits of insurance is the ability to provide expedient, tax-efficient cash to beneficiaries – when liquidity and speed are going to be most appreciated by those beneficiaries.

The tax code is an ever-evolving beast, and the intricacy of the code expands for high net worth and ultra high net worth individuals and their families. Even with the increases to the estate and lifetime gift tax exemption – currently $12.92 million for 2023 – a lot of tax exposure can be left on the table for many clients. Funded life insurance, particularly when placed in the proper trust vehicle, can increase the amount of one’s estate that is excluded from the estate and gift tax counter.

Insurance products’ features, options, and conversion abilities have also evolved greatly in recent years. In line with this trend, legal structures like trusts have adapted to be more inclusive of insurance as a primary or secondary funding mechanism. Wealth managers, especially those focused on existing asset management, are always appreciative of implementations that don’t interfere with their existing asset allocation mix and portfolio strategies. As a “bolt-on” inclusion to a current wealth management or estate plan, insurance is seen increasingly as a non-invasive way to improve client outcomes and tax efficiency.

Highlighting Growth Areas Within Insurance

We have seen sustained growth in the demand and purchase of individual long-term disability insurance in recent years. There is an often wide gap between the coverage provided by employers and the income needs a client would have if the policy was actually utilized.

And for small business owners, the need for widespread uptake of disability insurance is stark – according to surveys conducted by the Council for Disability Awareness and LIMRA, less than 15% of private U.S. workers currently have a long-term disability policy. An “own-occupation” disability policy offers protections for a business owner from the very real scenario where they can technically perform work of some kind, but not the specific job function that was the source of their high income.

Another growth area has been in tailored trusts to account for children or beneficiaries with special needs. Trusts can be structured with life insurance so that when monies are paid out, they are free from estate, gift, and income taxes. This fosters a seamless and unimpeded path to get the proceeds directed to the individual or caretakers who need it, without triggering any limitations to the individual with special needs to access Social Security and Medicaid benefits.

But far and away, the biggest pocket of growth, an area where we’re fielding questions from clients and advisors every day, is in long-term care insurance and protections. Powerful secular forces are driving this trend. The Baby Boomers will be the longest-living generation in world history, but most will also face a period requiring long-term care at some point in their lives.

Long-term care insurance sat quietly in the shadows for years, rarely implemented as a cornerstone piece of a financial plan. It’s something that society in general just wasn’t cognizant of before recent years. But now we’re at a time where longer average lifespans mean we have clients in their 40’s, 50’s, and 60’s who are caring for – or managing the care of – their elderly parents.

This reality frankly didn’t occur much in the 1960’s, 70’s, or 80’s, when their parents were at or near the age they are now. Back then, people generally weren’t living long enough to need long-term care. We were also more likely to see a case where 20 or30 years ago, one of the adult children wasn’t working, and so they could assist in the care of an elderly parent or parents.

Now we live in a time where more often than not, both the husband and the wife or both spouses are working and not necessarily available to take care of their parents. And yet they still have to; the impetus is still there to give that care. This inevitably causes extreme stress on the children, and while a lot of it is financial stress, it also carries over into their entire lives. They know that any free time they do have now has asterisks on it, as some of that time has to go to taking care of their parents.

As the client’s financial quarterback, it’s also important for advisors to be aware of the nuanced arc that a client has in their relationship with their parents. In the beginning, their parents brought them up and took care of them, and then when they became adults, they became friends with their parents. And that form of the relationship, as a friendship, is how they want the relationship to be preserved. But the unfortunate reality is that in many situations, the parent ends up in a situation where they can’t keep their dignity, due to the care that needs to be provided by their own adult children.

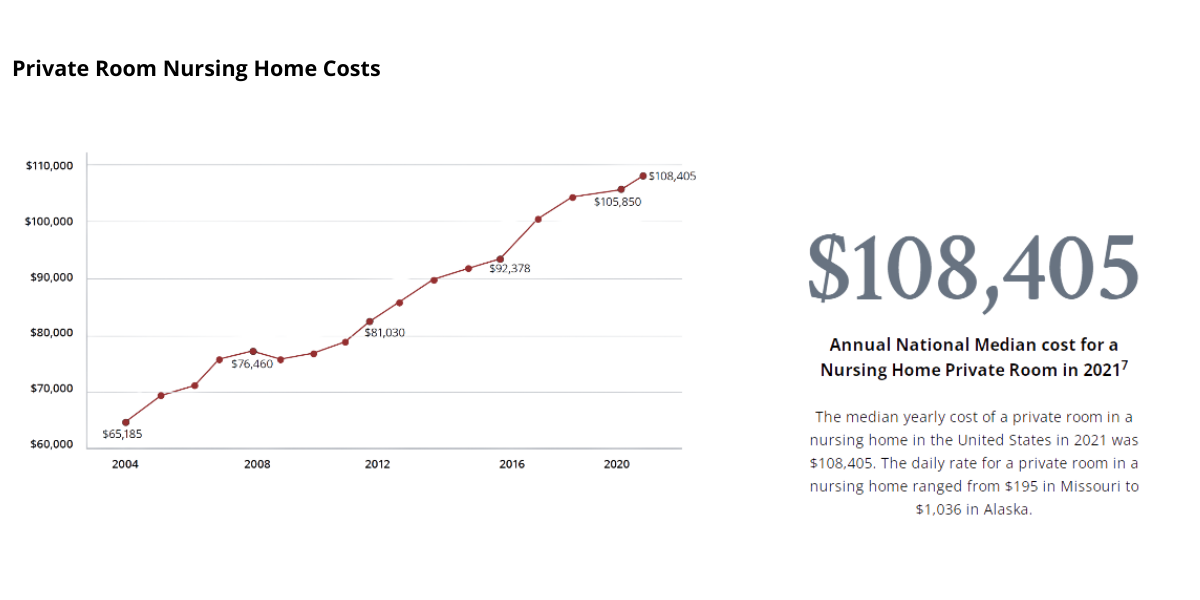

In the past, those who could provide for a long-term care facility typically did it in one of two ways. The first method forced them to spend down all of their parents’ assets to qualify for Medicaid – in which case any wealth they had generated and wanted to pass along is now gone. The only other option was to spend on long-term care or a nursing home out of pocket, which destroys a huge amount of wealth for the adult children, as long-term care facilities average over $100,000 per year in cost, with an average stay of over three years.

This creates scenarios where any client with $300k, $400k, or $500k in assets will end up spending that all down if they have a long-term care need. Data supports the truth that for anyone in their mid-60’s right now, there’s over a 60% chance that they’ll have a significant long-term care need in the future.

Talking Through LTC With Your Clients

With long-term care being such a large and growing issue, one that will touch nearly every client’s life at some point, it’s vital to have hard discussions with your clients. One silver lining is that these necessary discussions are becoming easier to have, as the issue of long-term care becomes more mainstream in society.

Your clients have learned from the experiences of their parents, their peers, and their own. They desire to better prepare and protect their children and beneficiaries from long-term care costs. And they also want to protect and preserve their wealth so they can follow through on their best-intended estate plans and pass on their legacy. And once a client is informed about the uses and flexibility of long-term care insurance, it’s not difficult to motivate them to implement a solution.

We know that your instincts and relationship with the client matter most. We don’t go into any discussion with another advisor with a lean toward long-term care insurance as a catch-all solution. We’ll follow your lead – the objectives and the plans you’ve already put in place. Maybe one of the children has the means and wants to pay out of pocket for their parent’s long-term care. Maybe that comes from a deep respect for what they saw their parents do themselves, and if an individual situation shapes up like that, it’s a fantastic and beautiful gesture. But it’s a plan, and more than anything else, we stress the importance of having the discussions with your clients and forming a plan. Insurance is the best answer for most, but not all, and we will always follow your lead on the right strategies to implement

As insurance professionals not tied to any carrier, acting independently in all cases, we have a unique vantage point to look out for trends in the industry. We work with advisors of all sizes, aiding clients of all ages and asset bases, whether as a spot request for a specific recommendation or to assist in crafting a modified wealth management plan.

Disclosures and Definitions

The information provided is for educational purposes only. The views expressed here are those of the author and may not represent the views of Leo Wealth. Neither Leo Wealth nor the author makes any warranty or representation as to the accuracy, completeness, or reliability of this information. Please be advised that this content may contain errors, is subject to revision at all times, and should not be relied upon for any purpose. Under no circumstances shall Leo Wealth be liable to you or anyone else for damage stemming from the use or misuse of this information. Neither Leo Wealth or the author offers legal or tax advice. Please consult the appropriate professional regarding your individual circumstance. Past performance is no guarantee of future results.