Japanese Capital Gains Tax for Foreigners

July 19, 2022

Thomas Y. Lu

The Japanese tax framework includes a capital gains tax, imposed on the profits made from the sale of any type of asset. Japanese nationals pay tax on worldwide capital gains, regardless of where the asset is located. However, the tax treatment for foreigners varies based on their residency status and the source of their income. For non-permanent residents, remittance of the gain (income) into Japan is also a factor. Tax matters related to visa and residency status are complex and foreigners planning to come to Japan for employment should seek professional advice in advance of their move and throughout their time in Japan to ensure tax compliance and efficiency.

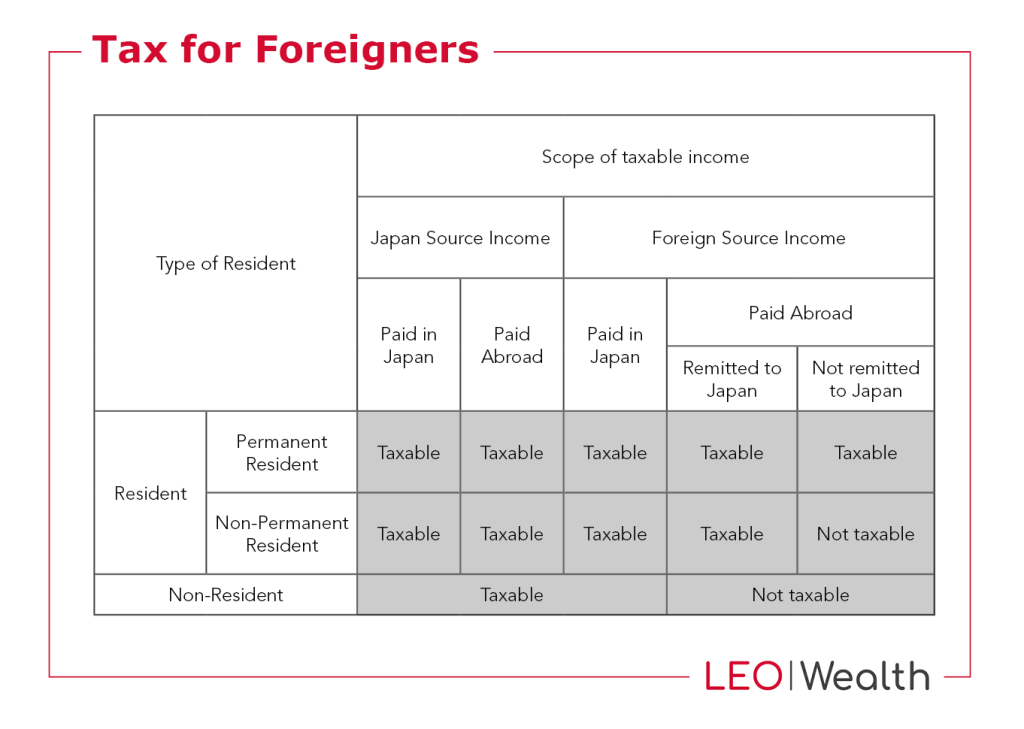

Japanese nationals are considered as permanent residents, regardless of time they may have spent living outside of Japan. Income that is generated in Japan, referred to as “Japan sourced” income, is subject to Japanese tax, regardless of the status of the recipient.

Any foreigner who has resided in Japan for an aggregate period of five years or more within the last ten years is also considered to be a permanent resident for income tax purposes, subject to full taxation on worldwide income and assets.

The table below outlines the treatment of different sources of income for different residency status. Remitted into Japan refers to electronically or physically bringing to Japan the gains or income in question.

* Non-permanent residents may be required to declare their foreign assets but in most cases are not subject to tax on foreign sourced income and capital gains that is not remitted into Japan. However, effective January 1, 2017, non-permanent residents will be taxed on sale of certain personal assets located outside of Japan even if not remitted into Japan (i.e., shares of securities bought and sold after January 1, 2017 while the taxpayer is a resident of Japan).

Any foreigner considering moving to Japan should seek professional advice with regards to the tax treatment of their income and assets. For U.S. citizens who are also taxed on worldwide income and assets, it is important to get qualified advice from tax professionals who understand the U.S. – Japan tax treaty and can provide guidance on reducing double taxation through treaty benefits.

Please contact our Tokyo based team of tax professionals to see how we can help.

DISCLAIMERS & DEFINITIONS

The information provided is for educational purposes only. The views expressed here are those of the author and may not represent the views of Leo Wealth. Neither Leo Wealth nor the author makes any warranty or representation as to the accuracy, completeness, or reliability of this information. Please be advised that this content may contain errors, is subject to revision at all times, and should not be relied upon for any purpose. Under no circumstances shall Leo Wealth be liable to you or anyone else for damage stemming from the use or misuse of this information. Neither Leo Wealth or the author offers legal or tax advice. Please consult the appropriate professional regarding your individual circumstance. Past performance is no guarantee of future results.