Japanese Estate Planning & Gift and Inheritance Tax Overview

September 2, 2022

Americans and other expatriates living in Japan face a complex and onerous system of probate and some of the world’s highest inheritance tax rates. Japanese estate planning is a complex subject that requires tailored advice for every situation. This article summarizes a few key considerations that may be helpful for families to understand as they engage with counsel for their Japanese estate and gift tax planning needs.

Planning Outcomes: No Will At All

Many local and international families in Japan do not have a will or do not use a will for their Japanese assets. While in certain circumstances, defaulting to the statutory inheritance tax framework as a method of administering a Japanese estate may be adequate, it’s important to consider the practical implications and the alternatives available to global citizens residing in Japan.

If a foreigner who owns or has rights to real estate property dies and the inheritance process begins, the laws of the decedent’s home country determine the heirs and the line of succession, as well as the division of the estate and matters regarding the acceptance and rejection of an inheritance. This means that if the decedent is a Japanese national, Japanese civil law determines these factors. If the decedent is a foreigner, usually the law of their home country applies even if the heirs are Japanese. Dual national cases are complex and require guidance from legal counsel with knowledge of both jurisdictions.

In each country’s international private law, the governing law for inheritance is determined by two systems: a unified system and a non-unified system. In a unified system, either the law of their home country, or the law of their country of domicile is applied exclusively. Japan, Germany and Taiwan follow this system.

In a non-unified system, the governing law depends on the type of asset involved. In the case of real estate, the law of the country in which the property is located applies. In the case of personal possessions, the law of the decedent’s country of domicile applies. The United States, France, and China follow this system.

Known for its strong and hard to override statutory inheritance framework, there is a very specific process and allocation that Japan uses to determine who receives assets from an estate. If your heirs are overseas, their relationship with you must be proven with official documents. If you do not have a Japanese family registry, you will need to obtain official documents from overseas to prove family relationships. Claiming the inheritance of decadents from countries without a family registry system adds a layer of complexity, and usually requires an affidavit from a public notary. In this case, the amount of time, cost, and complexity it takes to complete inheritance procedures can increase significantly.

Statutory asset division under Japan law:

- If the heirs are your spouse and children: your spouse will receive half and the children half.

- If the heirs are your spouse and direct ascendants: your spouse will receive 2/3 and the direct ascendants will receive 1/3.

- If the heirs are your spouse and siblings: your spouse will receive 3/4 and your siblings will receive 1/4.

Statutory heirs:

- Your Spouse. It is generally not possible to disinherit your spouse.

- First line of succession: Your Children

- Including adopted and biological children

- Illegitimate children born outside of the marriage generally have the same inheritance rights as legitimate children.

- Second line of succession: Your Parents

- If your parents have pre-deceased you, then the rights to your inheritance go to your grandparents, and if your parents and grandparents have already passed away then the rights to your inheritance go to your great-grandparents.

- Third line of succession: Your Siblings

- If your siblings have pre-deceased you, then your inheritance is passed on to your niece or nephews.

If you die without heirs, the court will appoint an administrator of inherited property to manage your estate and determine heirship and asset distribution.

Planning Outcomes: Secret Will

It is possible to create a secret will. Typically for a secret will, the location is known but the contents are not. A secret certificate will is created by the testator by sealing an envelope containing the will in front of a notary public, but its contents inside the will itself are kept a secret. Like a holographic will, its validity may be contested because the contents of the will are not discussed, documented or confirmed by the notary public or any other official witness.

Planning Outcomes: Notarized Wills

A notarized will is the most common and most practical solution for many families. By using an accredited Japanese notary public who documents both the contents of the will and the execution of it by the testator, there is little room to argue about the validity or the contents. Using a will done by a notary public also means the inheritance process can be completed without having to go through probate procedures in the Japan court system in most cases. An original certified copy of the notarized will is stored at the notary public’s office and is registered in a nationwide database.

Planning Outcomes: Holographic Will

A holographic or hand-written will can be valid in Japan but it is usually inferior to a will completed by a notary public. If a family member is known to have created a holographic will, it should be discussed with counsel if a notarized will should be done to replace it. Once a handwritten will is located, it must go through the probate process. If the will is sealed, it must be unsealed with the heirs in attendance, in front of an officer of the family court as part of the probate process. For wills not written in Japanese an official translation should be provided.

Planning for Families in Japan

Japanese estate planning is complex and the needs of global citizens with foreign assets or non-Japanese nationals living in Japan should be explored carefully with qualified counsel prior to creating any wills, trusts or other estate planning documents. Our team of experienced tax and estate advisers can assist you with selecting counsel and supporting you through the global estate planning process.

Let’s take a deeper dive at how Japan inheritance tax works and look at how it would be calculated.

What Can Be Inherited?

In general, inheritance taxes apply to property, money, or assets. The following types of properties might be included in a Japanese inheritance:

- Bank deposits

- Loans

- Shares in a bond or company

- Insurance proceeds

- Retirement allowances

- Investment interest

- Japanese government bonds or foreign government bonds

- Patents, copyrights, and trademarks

- Ship or aircraft

Your tax liability is based on the fair market value of the inherited assets at the time of death, minus funeral expenses, liabilities (including mortgages), and certain exemptions.

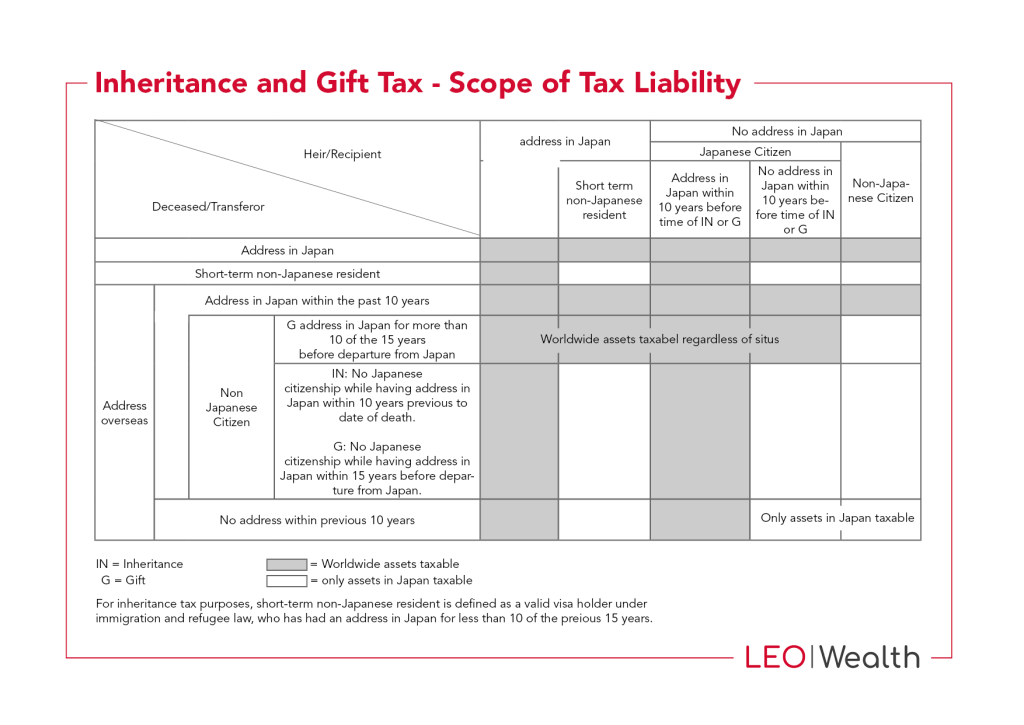

Who is Subject to It?

For Japanese nationals, if the heir has a jusho (住所) (which may be loosely translated as having a domicile) in Japan at the time of receiving the inheritance, he/she will be subject to Japan inheritance taxation. In addition, if the decedent is also a Japanese national with a jusho in Japan at the time of passing, Japanese inheritance tax will also apply to the heir regardless of his/her jusho status or nationality. For Japanese nationals, they would still be considered as having a jusho for Japan gift/inheritance tax purpose for 10 years even after breaking Japan tax residency.

Effective April 1, 2017, the transfer of non-Japan situs assets between non-Japanese nationals who have a jusho in Japan for less than 10 years out of the last 15 years and also holding a Table 1 visa (‘short-term resident’), with other short-term residents, is exempt from Japan gift and inheritance tax.

The short-term resident needs to meet the following requirements in order to be exempted. The non-Japanese national has to have a jusho in Japan for not more than 10 years out of the past 15 years and also hold a Table 1 visa. Non-Japanese nationals who satisfy the above time test, but not the visa test will not qualify as short-term residents and will therefore be subject to taxation of Japan gift and inheritance tax on worldwide assets while residing in Japan.

A Table 1 visa includes work related visas and does not include the permanent resident, spouse or child of Japanese national, spouse or child of permanent resident, and long-term resident.

Effective April 1, 2021, the Japan gift and inheritance tax laws were updated to provide further relief to non-Japanese nationals. The transfer of non-Japan situs assets from non-Japanese nationals to other non-Japanese national short-term residents is exempted from Japan gift and inheritance tax if the non-Japanese transferor holds a Table 1 visa.

The exemption with the time test mentioned above in Japan does not apply to non-Japanese resident recipients of gifts and inheritances of non-Japan situs assets. Non-Japanese resident recipients still need to have had jusho in Japan of not more than 10 years out of the past 15 years and hold a Table 1 visa in order to be considered as short-term residents and be exempt from Japan gift and inheritance tax on non-Japan situs assets received from non-Japanese national transferors.

Any Japan situs assets will be subject to Japan gift and inheritance tax, regardless of whom or when the transfers take place.

How will it be Taxed?

Assets subject to inheritance tax include tangible, intangible, real, or personal property, unless otherwise specifically exempt under the law. The asset is valued in accordance with the provisions of the Japanese tax rules. The same rules apply to the gift tax system.

In Japan, it’s not the estate that’s taxed, but the heirs themselves—and the number of heirs factors heavily into the overall calculation. The total amount due is calculated based on the statutory amount due to each heir, regardless of whether the heir receives that amount or not—so you also can’t fudge the totals by writing people out of a will. The final payment is divided among the actual recipients, so even if the will cuts someone out, it’s the recipients who have to pay the tax amount.

The intestacy shares depending on who the heirs are. For example:

If the decedent is survived by his/her spouse and two children,

Spouse: ½, children: ½ (equally)

If the decedent is survived by his/her spouse and parents,

Spouse: 2/3, parents: 1/3 (equally)

If the decedent is survived by his/her spouse and siblings,

Spouse: ¾, siblings: ¼ (equally)

The most basic statutory calculation allots 50% of inherited assets to a surviving spouse and 50% in total to surviving children, divided equally among them

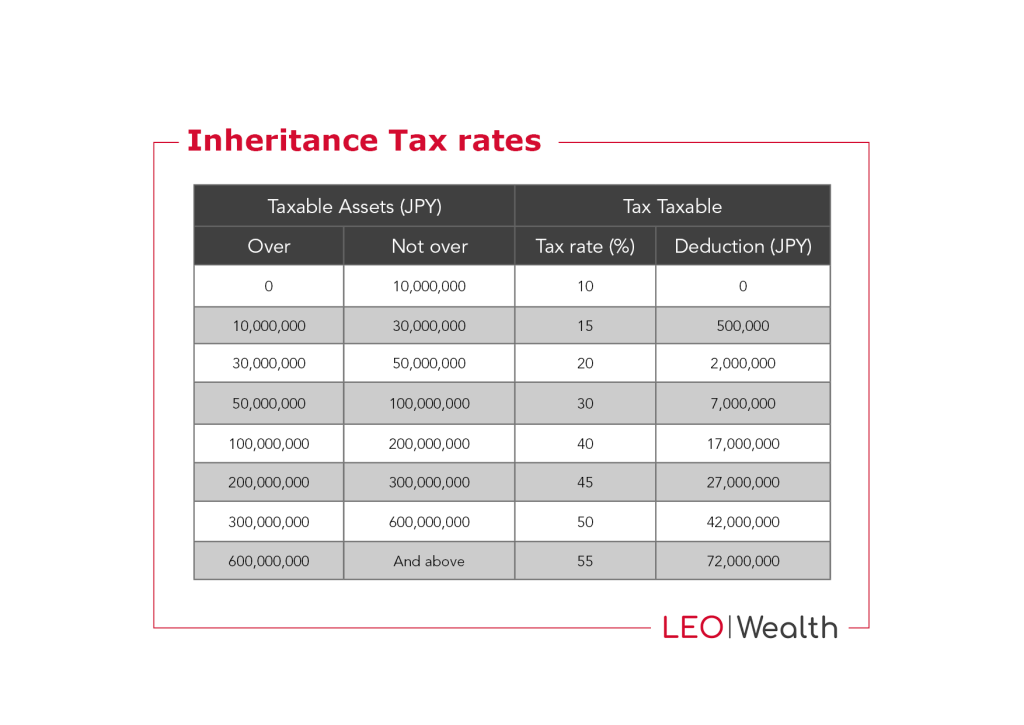

Once the number and nature of statutory heirs is determined, the aggregated tax base is then divided among all statutory heirs, and the inheritance tax rate in the table below is applied to each total. Thus, the tax rate is not applied to the gross aggregated tax base, but to the fraction received by each heir—meaning you will likely face lower rates, assuming there is more than one statutory heir.

Basic Exemptions/Credits

The following properties are considered tax-exempt:

Effective January 1, 2015, the amount of basic exemption is JPY 30 million plus JPY 6 million multiplied by the number of statutory heirs. Other deductions include:

- Family altars, graves, rituals.

- Donations to local government, charitable institutions and foundations.

- Life insurance proceeds up to JPY 5 million per statutory heir.

- Retirement allowance up to JPY 5 million per statutory heir.

Mortgage from real estate properties can be deducted from the assessed property value. Thus, if you a large amount of mortgage and pass it on to your heirs, you can actually get a very low or negative property value when it comes to gift or inheritance taxes.

Foreign tax credits depending on if the same asset is also taxed from another tax jurisdictions.

Minors credit – JPY 100,000 multiplied by the heir’s age for minor heirs under the age of 20.

Disability credit – JPY 100,000 multiplied by the heir’s age for heirs with disabilities (JPY 200,000 for special disabilities).

Spousal credit – Unlike the unlimited marital deduction in the United States, the spousal credit for the Japanese inheritance tax is limited. The spousal credit would mean no Japanese inheritance tax will be imposed on amounts that the spouse receives up to the greater of: (1) the spouse’s statutory share of the total taxable assets (typically ½), and (2) JPY 160 million.

When do I Need to File and Pay My Inheritance Tax?

Inheritance tax return must be filed and taxes paid in one lump sum within 10 months of the date of death. Payments can be made at the tax office or post office, and you may also pay through an appointed local tax representative. There are penalties for late payment, understatement and non-payment, which increase further if it is discovered during an audit.

Japan Gift Taxation

Taxation Methods for Gift Tax

Gift tax has two taxation methods: calendar year taxation and taxation for settlement at the time of inheritance.

Calendar Year Taxation

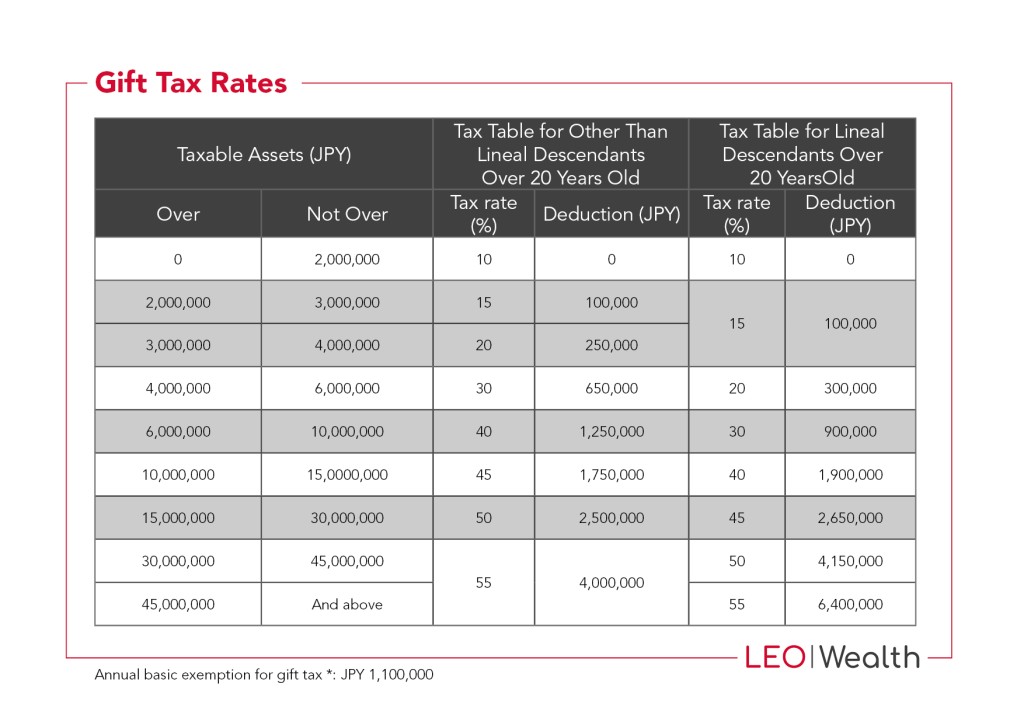

Donated properties whose value exceed the basic exemption of 1.1 million yen per donee/per year are subject to gift tax. This covers the total value of all items received from January 1 to December 31 of that year. Gift tax will not be imposed if the total value of the items donated to you in a year do not exceed the basic exemption – that is, you are not required to report and file a return for gift tax in this case.

Who is Subject to It?

Japan gift taxation follows the same as inheritance tax law so please refer to the above section.

Taxation by Settlement at The Time of Inheritance

In this system, the gift tax is imposed after the total value of the properties donated in a calendar year are subjected to a special deduction of 25 million yen. The taxpayer can apply for the deduction when he or she files a return for the gift tax by a particular due date prescribed by law.

This system is applied when parents or grandparents aged 60 years and older donate property to their grandchildren or children who are at least 20 years old. To select this system of taxation, the taxpayer needs to file a return for gift tax between February 1 and March 15 of the following year.

Once the taxpayer selects this system, it will be applied to all properties donated by the same donor from the year when it was selected. Once you select this system, you cannot change it to a calendar year taxation system. Should the donor pass away, an inheritance tax will be computed by adding the market value of the properties at the time of donation to the value of the estate.

Eligibility

As earlier mentioned, for one to be able to select the taxation system for settlement at the time of inheritance, the donor must be parents or grandparents who are at least 60 years and the receiver is also the presumptive heir or grandchildren of the donor’s children or grandchildren. The receiver should be at least 20 years as of January 1 of the year when the property will be handed over for donation.

There are no restrictions as to the type of properties or assets that can go under this system. The donor may also donate any value of a property as frequently as needed.

Calculating the Tax Payment

Under this system, the inheritance tax is derived from deducting the amount of the gift tax that has been paid previously from the amount of the inheritance tax when the donor passed away. The inheritance tax is based on the sum of the value of the properties that were donated and the value of the properties acquired by bequest or inheritance.

Application of the Taxation System for Settlement at the Time of Inheritance

The recipients of the property are required to submit the “Report on the Selection of the Taxation System for Settlement at the Time of Inheritance” to the Tax Office which has jurisdiction over their address.

Filing the Tax Return and Payment

The person receiving the donation must file a return and pay the gift tax between February 1 and March 15 of the following year. It is also still necessary to file a return by these dates even when there is no tax to be paid particularly if the individual elects for the taxation system for settlement at the time of inheritance.

Taxes are generally paid in cash but individuals may apply for postponement of tax payment. This allows the taxpayer to pay the amount due in instalments over a set number of years. To postpone tax payment, he or she must submit the pertinent application forms and other supporting documents to the District Director of the Tax Office by a certain due date for special approval.

Exemption for Spouse

A residential property or money that is to be used for purchasing residential property may be subject to a special provision when donated between a couple who have been married at least 20 years. This special provision includes a basic exemption of 1.1 million yen and up to 20 million yen (exemption for spouse).

Application Requirements

To be eligible for this special provision, the following requirements must be fulfilled:

The asset was donated between a couple after they have been married for more than 20 years

Upon receipt of the donation, the recipient should live in the property that was acquired by donation my March 15 of the year following the year of donation. He or she should continue to live in the said residential property.

This special exemption for spouses can only be used once from the same spouse.

Applying for the Special Provision

To apply for the special exemption, the recipient should file a return for the gift tax and attach the following documents:

- Family register or an extract that was created within ten days from the date of receipt of the donation

- Copy of the supplementary family register

- Certificate of registered information of the property and other supporting documents that certify that the recipient has acquired a residential property

- If the actual residential property was received, the recipient should also attach the certificate of fixed asset evaluation and other similar documents.

Japan gift and inheritance tax calculations are complex and involves many factors. Please consult with your trusted tax advisor to prepare an estimated Japan/US inheritance/estate tax or gift tax projections in order to get a better understanding of your overall tax exposure at the time of the asset transfer.

DISCLAIMERS & DEFINITIONS

The information provided is for educational purposes only. The views expressed here are those of the author and may not represent the views of Leo Wealth. Neither Leo Wealth nor the author makes any warranty or representation as to the accuracy, completeness, or reliability of this information. Please be advised that this content may contain errors, is subject to revision at all times, and should not be relied upon for any purpose. Under no circumstances shall Leo Wealth be liable to you or anyone else for damage stemming from the use or misuse of this information. Neither Leo Wealth or the author offers legal or tax advice. Please consult the appropriate professional regarding your individual circumstance. Past performance is no guarantee of future results.